Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

You have found your dream home. It’s the exact size and look you wanted, and even better, it’s within your price range. But when you take a closer look at the total cost with your real estate agent, you notice an unexpected monthly fee that can add up to an extra thousands per year: a homeowners association (HOA) fee. What is it? Can you negotiate it? And most importantly: is it worth it?

This a situation many home buyers find themselves in: learning about homeowner association fees and whether or not they are worth the cost. Some homeowners, though, purchase the property and don’t take these fees into account — and have buyers remorse months or even years down the road.

Before you decide to buy a property — whether that’s a house, a condo, or a townhome — that requires HOA fees, there are several factors to consider, such as what they cover, their cost, the penalties involved and more — all things that we will cover in this article to help you decide if HOA fees are truly best for you.

What Are HOA Fees?

Let’s begin by answering the question: “what are HOA fees?” It starts with understanding what a homeowners association is.

A homeowner’s association (HOA) is an organization with a centralized governing structure — such as a board of directors — whose roles are to enhance communities and quality of life by providing facilities and amenities.

These facilities and enhancement cost money, which the homeowners are required to pay for. That’s where the HOA fee comes in.

There is no negotiating with HOA fees — what the HOA asks you to pay, you must pay.

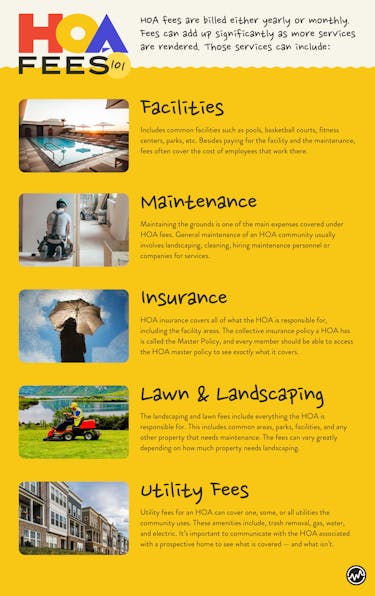

HOA fees are billed either yearly or monthly. Fees can add up significantly as more services are rendered. Those services can include:

- Facilities

- Maintenance

- Insurance

- Lawn and Landscaping

- Utility fees

We’ll look at each one in-depth next to lift the veil on what you’re paying for when you pay HOA fees — that way you’ll have an answer to the question “what are HOA fees?”

Facilities

The most common facilities that require HOA fees are:

- Swimming Pool(s)

- Tennis / Basketball Courts

- Fitness Center

- Community Center

- Parks

- Parking Lots

- Security

An HOA may have some or even more facilities than listed above.

Besides paying for the facility and the maintenance, fees often cover the cost of employees that work there. This is why HOA fees can be costly.

Maintenance

Maintaining the grounds is one of the main expenses covered under HOA fees.

General maintenance of an HOA community usually involves:

- landscaping

- cleaning

- hiring maintenance personnel or companies for services

Insurance

Insurance is included in many HOA fees. HOA insurance covers all of what the HOA is responsible for, including the facility areas.

The collective insurance policy a HOA has is called the Master Policy, and every member should be able to access the HOA master policy to see exactly what it covers.

This is important because homeowner’s or renter’s insurance should supplement the master policy. That way, homeowners can be safe and ensure that everything is covered.

There are typically two kinds of HOA master policies:

Bare Walls-In Coverage

This type of coverage insures the building itself, all the way to the drywalling. So, it is strictly for building coverage, and doesn’t include anything inside a dwelling such as your furniture.

All-In Coverage

This type of coverage insures everything that isn’t considered a personal belonging of the homeowner or tenant. It will include insurance for kitchen appliances, counters, electrical, and everything else within the building and dwellings that are considered part of the building itself.

What if you don’t plan on using the insurance that is covered by the HOA fee? You still have to pay for it, just like you’ll be paying for the maintenance and repairs.

When you buy a property with HOA fees, you need to purchase insurance that aligns with the master policy.

Homeowner’s and Renter’s Insurance and HOA Master Policy Supplementation

When you’re shopping for condo coverage or homeowner’s insurance, your mortgage lender will have specific rules it requires its customers to follow regarding how much insurance to have.

The goal is to obtain coverage that will satisfy your mortgage lender and to have that policy complement the HOA insurance master policy perfectly.

Yes, you can be overpaying for insurance, and that’s one thing that you will want to avoid. If you know what kind of policy your HOA has, you should be able to work with your personal insurance company to create a policy that works for you and ensures that everything is covered.

The best way to find the best rate is to get a quote from multiple insurance companies — including local and nationwide companies. Also, make sure to talk to your homeowner's association about what companies they work with for insurance.

HOA Insurance for Single-Family or Subdivision Homes

If you buy a house and it comes with an HOA, the insurance is a bit different than an HOA for a condominium property or high-rises. The HOA insurance doesn’t extend to the home or any other buildings on the property.

The single-family home will always be insured by the homeowner, where most of the repairs and the building’s maintenance will be the homeowner’s responsibility.

Lawn and Landscaping

The fees can vary greatly depending on how much property needs landscaping. In a condominium setting, there will likely be more landscaping done versus a multiple-dwelling building.

In an HOA that has only single-family homes, the homeowners will likely be responsible for the lawn, and there are some serious rules regarding lawn care and landscaping that you should ask about.

However, your HOA will be allowed to enter your property as they see fit, and they can mow your lawn or hire a landscaping company to work on your property if it’s included in the contract.

The landscaping and lawn fees include everything the HOA is responsible for. This includes common areas, parks, facilities, and any other property that needs maintenance. Remember: even if you do not set foot on any of the lawns your HOA is responsible for, you will still be required to pay the fees for their maintenance.

Utility Fees

Utility fees for an HOA can cover one, some, or all utilities the community uses. These amenities include:

- trash removal

- gas

- water

- electric

Some homeowners prefer their HOA to handle items like this. It’s important to communicate with the HOA associated with a prospective home to see what is covered — and what isn’t.

While your realtor should be able to get all the information for you, it can be good to get the information first-hand so that there aren’t any miscommunications.

How Much Do HOA Fees Cost?

Every HOA is different, and some associations in areas with members who have a large income can charge upwards of $700 – $1,000 per month, while some will only charge around $100 per month.

On average, most people will pay around $200 to $300 per month in HOA fees.

Though this is the average today, keep in mind that the final cost in fees per month depends on the HOA. Because of that, the fees can increase at any time for any reason.

And if you don’t pay the fees, you can face serious penalties.

HOA Fee Penalties

Fines can incur for anything written in the HOA rules. You can be fined for:

- paying fees late

- not mowing your lawn

- not removing decorations

- playing your music too loud

If you decide not to pay your fines, your HOA can sue you for the money, plus interest and legal fees, which can get significantly expensive.

The HOA can also sue you for not paying dues and fees. A court can settle the matter, and even garnish your wages.

There are also laws in place in which not paying your HOA fees can result in extreme measures like putting a lien on your home, where it will go into foreclosure.

An HOA cannot directly kick you out of the home and out of the HOA, but there are many ways that they can indirectly, through legal means, and will go through great lengths to ensure every member pays their share.

Should You Buy A Property With HOA Fees?

Buying a home, condo, townhouse, or an apartment is a big decision, and some portions of the contract can easily slip by you during the exciting buying process.

At first, HOA fees may not seem like much. Plus, most HOA’s exist to provide a better living for the community.

However, there are many cases in which buying a house without an HOA associated with it would be just as costly, if not cheaper, than buying a condo, townhome, or apartment with HOA fees.

The only way to get out of an HOA clean is to keep current on all fees, fines, and dues, then sell your home and move. Otherwise, you are stuck with them — whether you like it or not.

To decide if you should buy a property with HOA fees, ask yourselves these questions:

- Do you want or need the amenities and facilities and parking that an HOA can give you? Or can you find cheaper alternatives (for example, instead of paying an HOA fee for a neighborhood gym, you can create your own workout plan)

- Do you want or need an association to pay your bills for you?

- Do you want to give an HOA unrestricted access to your home and property?

Homeowners associations exist for a reason, and there are a lot of people that enjoy having them, so first you must find out if you would benefit from being a part of one.

If you are debating whether to buy a property with HOA fees versus a property without HOA fees, consider that you could use the HOA fee money to instead:

- Replenish your emergency fund

- Invest the money — and let it work for you

- Boost your savings

- Start the business you’ve dreamed about

The Bottom Line: What Are HOA Fees?

Now that you know the answer to the question “what are hoa fees”, If you find your dream home, but it comes with HOA fees, do the math to decide how much it’ll cost long term before signing on the dotted line. Doing so can save you money now and down the road — and help you on your path towards financial freedom.