The Ultimate Deal Analysis Worksheet

In This Article

Most people invest in real estate with the hope of generating wealth. While the average investor isn’t expecting to make millions overnight, they are looking to do something smart with their money. They’re looking in the right place.

There are tremendous opportunities to generate wealth in real estate investing. Real estate investing is all about making smart decisions and taking strategic risks.

One of the smartest decisions and most strategic risks you can make it called leveraging.

What is leveraging?

When you leverage, you’re borrowing money to help finance a property investment. The most common means of leveraging in real estate is taking out a mortgage. With a mortgage, you’re borrowing from the bank to purchase your home.

Leveraging gets more interesting when you apply it to investment properties. You’re buying these properties with the expectation of a financial return, so you’ll need to structure your leveraging strategy in a way that maximizes that return.

In order to structure your leveraging strategy, you’ll need to know the logistics of leveraging and what this strategy has to offer.

There are two main benefits to leveraging that you need to know . . .

Benefit 1: Return on Investment (ROI)

The most obvious benefit of leveraging is that you aren’t paying out of pocket. This is especially helpful if you don’t have much of your own money to invest but want to get into the real estate game nonetheless.

But there’s an even bigger benefit to leveraging, and it requires some explaining. Here’s an example:

Let’s say you buy a rental property for $100,000 and you rent it out at $1,000 per month.

Scenario 1: All-Cash Purchase

So, you decide not to leverage real estate. You purchase the property in all cash.

After paying property taxes and insurance and miscellaneous expenses each month, let’s say you take home $700 every month of that $1,000. $700 is your monthly cash flow.

Scenario 2: Leveraged Purchase

You finance the property with a conventional mortgage, putting 20% down. That’s $20,000.

You pay the same expenses every month as you would with the all-cash purchase, but now you also have a mortgage to pay off.

If you’re paying each month with a 5% interest rate, you’re making a mortgage payment of $430 per month. Instead of taking home $700 per month as with the all-cash purchase, you’re taking home $270 per month.

So, Which Looks Better?

It seems like you’re making more money if you purchase in all-cash. You’re taking home $700 per month instead of just $270. If you think this an all-cash investment is the obvious answer, think again.

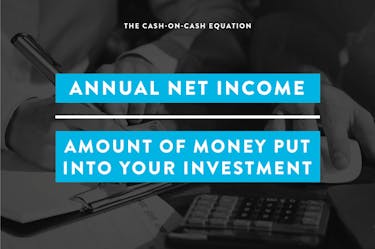

What matters in real estate investing isn’t the cold numbers. What matters is how much money you are making on the money you invest. You want to know how much cash you are making in relation to how much cash you put in. This is determined using the cash-on-cash equation.

Let’s look at those scenarios again.

Scenario 1: All-Cash Purchase

Your net monthly income is $700 after expenses. To get your annual net income, multiply by 12. Then divide it by your initial investment of $100,000.

It should look like this:

($700 x 12)/$100,000 = 0.084 = 8.4%

That’s 8.4% cash-on-cash return.

Scenario 2: Leveraged Purchase

Your net monthly income is $270 after expenses and mortgage payments. Again, multiply this by the 12 months in the year for your annual net income. Then divide it by your down payment of $20,000.

It should look like this:

($270 x 12)/$20,000 = 0.162 = 16.2%

With a leveraged purchase, you’re making 16.2% cash-on-cash return.

So, Which Looks Better NOW?

Do you see the difference?

The leveraged purchase provides nearly double the return on the money you invested. While your monthly cash flow seemed significantly lower at first glance, you’re actually getting double the return on your investment.

Look at the change. The cash-on-cash equation helps you determine how much of a return you’re really making when you take your actual investment into account. Cash flow means nothing when you don’t consider your investment.

A leveraged property won’t always offer double the return on your investment. It all depends on your initial investment, monthly payments, and cash flow. In some cases, a leveraged real estate investment could give you negative returns while an all-cash investment puts you in the positive.

What matters is that you’re able to run the numbers on your investment.

Benefit 2: Quantity of Investments (Get More for Less)

There’s another benefit to leveraging—and it’s staring you right in the face.

In the all-cash scenario, you spent $100,000 of your own money. In the leveraging scenario, you only had to spend $20,000 of your investable money.

Let’s assume you have that $100,000 to invest in both scenarios. There are 5 sums of $20,000 in $100,000. This means that instead of buying one property for $100,000, you could potentially leverage 5 properties.

That’s right. You can either pay all-cash for one property in Scenario 1 or you can finance 5 properties with Scenario 2.

Before you decide, let’s look at the benefits of financing 5 properties:

Higher total monthly cash flow

Let’s return to our cash-on-cash calculations. We know that if you pay all-cash for a $100,000 property, your cash return is going to be $700.

If you own 5 properties and make $250 off each of them every month, your monthly cash return is going to be $1,350.

But we know not to trust only cash value, so let’s run the numbers through the cash-on-cash calculation.

We know from the example above that our all-cash purchase delivers 8.4% cash-on-cash return.

For our 5 investment properties, the calculation would be: $1,350 x 12 / $100,000 = .162. This means there’s still a 16.2% return on your investment with your 5 properties—and you have more cash value to boot.

5 times the appreciation benefits (when applicable)

If a house appreciates, that’s basically free money for you. So if a $100,000 real estate investment appreciates $30,000, you make $30,000 of what’s essentially free money.

If your all-cash purchase property gains $30,000 in appreciation, you’ve gotten a bonus $30,000 in your pocket.

But if you own five properties and they all gain the same $30,000 in appreciation? You have a bonus of $150,000 in your pocket—5 times that $30,000.

Note: Numbers being used are solely to illustrate the math and are not actual numbers. All equations should be run off actual property numbers and never estimated. Also, $100,000 buying five properties does not take into consideration closing costs with the lender and other expenses to buy the property.

5 times the tax benefits (which are huge)

Tax benefits are less intuitive to calculate, but they are substantial on rental properties. With your 5 properties, your tax benefits are higher than what they would be on just one property,

Diversification

So, you picked a bad property. If you made an all-cash payment, that money would essentially be sunk. You’d be taking losses over and over again.

With 5 leveraged properties, all of your eggs aren’t in one basket in case you pick a lemon property.

Offset against vacancy and repairs

If you invest in one house and your tenants move out, you have to cover vacancy and repair expenses yourself. If the tenants in one house move out but you own five houses, you can use the income from the other four houses to offset those expenses.

With all of those benefits, what’s the catch? Why isn’t everyone leveraging like mad?

Leveraging vs. All-Cash: The Debate

After exploring the benefits of leveraging, you might think the answer to this debate is an obvious one. Shouldn’t leveraging win out over paying all-cash for an investment property?

The reality is that there are a lot of people shouting from the rooftops that leveraging is dangerous and risky and should be avoided at all costs.

So what’s the real problem leveraging? The main reason is fear. People are afraid of leveraging. Here are some of the main fears:

But the fear surrounding leveraging is based on misunderstandings. Let’s re-examine the list of possible fears, but follow-up with easy and practical solutions:

They fear not being able to cover the mortgage payments on their properties and being foreclosed upon.

This is why having a nest egg is important. Having money saved up can save you a ton of grief here.

As mentioned above, having more than one cash-flowing property can also help offset the expenses of another property.

Or, if you initially had $100,000 of investable cash, you’d be wise to set some of that aside for just this emergency scenario.

They don’t want the bank in control of their asset.

Technically, the bank can take your property—but legally they can only do that if you don’t make the payments you agreed to in your contract. If you’re making your payments, the bank can’t do anything to your property and you are legally in control.

Plus, even if you pay for the property in full, you still aren’t 100% in control. You still owe property taxes. If you don’t pay those, your property can be taken.

They fear interest rates rising.

This is only a danger on adjustable-rate loans. Fixed loans should always be used for this exact reason. Loans with balloon payments pose the same risk.

They fear becoming overleveraged and being unable to manage their investments.

Just because leveraging has benefits does not mean that it should be done without any consideration. You should be smart in all of your financial decisions, and this is no exception.

Being irresponsible is just that: irresponsible. If you don’t have a plan to support your investments or knowledge of what you’re doing, you have no business making investments in the first place.

The key is to run the numbers on the properties you buy. Make sure they can support your loans. And again: have a nest egg.

They fear assumed appreciation falling short and leaving them empty-handed.

Monthly cash flow on a property is crucial. If your property doesn’t cash flow, you should have a plan in place for covering your loans every month. A backup fund is also advised.

The debate between paying all-cash for a property or leveraging a property is not one with a right or wrong answer. Both methods can offer you financial gains via your real estate investment on a solid property.

It’s also highly situation-dependent. Some situations may favor paying cash versus leveraging or vice versa. Now that you know how to crunch the numbers and weigh your options, you should be able to predict the return you’ll see on your real estate investments and make the right decision.

Now Leverage Your Success

At the end of the day, you need to feel comfortable in the investments you make with your money. No matter how promising the numbers are, some people will never be able to sleep knowing they have loans out on their properties. And no investment, no matter how great, is worth financial stress and losing your peace of mind.

But remember: your worst case scenario is foreclosing on a property. When you lose a property, you lose your down payment and points on your credit score. This can be scary, but it isn’t the end of the world.

With basic and responsible planning on the part of the investor, leveraging might be the best real estate decision you ever make.