Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

Have you fallen in love with a house that despite it’s rough exterior, it “has potential”? If you’re looking for a new home to live or invest in, buying a fixer upper is a unique option that has significant advantages.

Aside from being able to purchase the home at a lower price, you can also remodel it to its “full potential”, such as installing a new kitchen, updating the floor plan, maybe even putting in a pool ... all of which can increase the home’s value.

But these renovations can be costly — often tens of thousands of dollars.

What’s more, a conventional mortgage won’t cover these costs.

So if you want to buy a home and remodel it, how can you pay for the renovations?

That’s where rehab loans come in.

So what are your rehab loan options? And more importantly, which one is right for you?

In this article, we will break down:

- What rehab loans are and how they work

- Pros and cons of each rehab loan

- The one type of loan you should avoid at all costs

- How to choose the right type of rehab loan

If you’re ready to learn about rehab loans, let’s get started!

Why Rehab Loans Exist

Let’s imagine that you’re interested in a house listed for $200,000. After some research, you think you’ll need $50,000 on top of that for renovations to the house.

With a conventional mortgage, your lender is not going to approve a $250,000 loan to buy a house that is appraising at $200,000.

If you don’t have the extra cash to make the renovations before moving in — whether that’s renovations you simply want or renovations that are required — what can you do?

A rehab loan can be the solution.

The loan addresses a common problem when buying a home that needs renovation: lenders often don’t approve loans for homes in need of major repairs.

What Are Rehab Loans?

A rehab loan allows you to finance the purchase price as well as needed or wanted repairs in the same loan.

With a rehab loan, there’s peace of mind because you’re not left wondering if you’ll have all of the money to make renovations.

Plus, by using a rehab loan, you won’t have to empty your savings account or put home renovations on a high-interest credit card.

Types of Rehab Loans

Next, we’ll explore types of rehab loans you can choose from. This includes:

- FHA 203(k) Loan (Limited or Standard)

- Fannie Mae’s HomeReady Loan

FHA 203(k) Loan

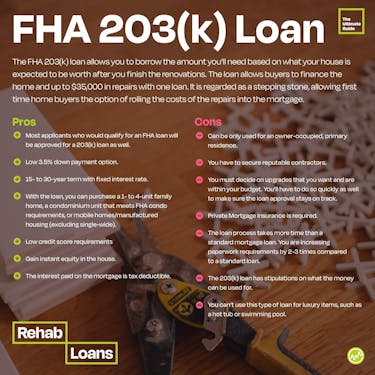

A FHA 203(k) loan allows you to borrow the amount you’ll need based on what your house is expected to be worth after you finish the renovations.

The loan allows buyers to finance the home and up to $35,000 in repairs with one loan.

The FHA 203(k) loan is regarded as a stepping stone, allowing first time home buyers the option of rolling the costs of the repairs into the mortgage.

Pros

- Most applicants who would qualify for an FHA loan will be approved for a 203(k) loan as well.

- Low 3.5% down payment option.

- 15- to 30-year term with fixed interest rate.

- With the loan, you can purchase a one- to four-unit family home, a condominium unit that meets FHA condo requirements, or mobile homes/manufactured housing (excluding single-wide).

- Low credit score requirements: you could potentially qualify for an with a credit score as low as 580, although most FHA-approved lenders won’t accept anything below 620.

- gain instant equity in the house.

- The interest paid on the mortgage (money that is borrowed to buy the home and repairs) is tax deductible.

Cons

- Can be only used for an owner-occupied, primary residence.

- You have to secure reputable contractors.

- You must decide on upgrades that you want and are within your budget. You’ll have to do so quickly as well to make sure the loan approval stays on track.

- Private Mortgage Insurance is required.

- The loan process takes more time than a standard mortgage loan. You are increasing paperwork requirements by 2-3 times compared to a standard loan.

- The 203(k) loan has stipulations on what the money can be used for.

- You can’t use this type of loan for luxury items, such as a hot tub or swimming pool.

There are two types of FHA 203(k) loans: Limited and Standard. Next, we’ll look at each in depth.

Limited Vs Standard FHA 203(k) loan

Limited 203(k)

The Limited 203(k) Loan is used for minor modeling and non-structural repairs — keep in mind that with the Limited 203(k) proceeds may not be used to finance major renovations.

For example, eligible improvements include:

- Repairing/replacing plumbing, heating, AC, and electrical systems

- Repairing or installing new roofing

- Installing a new refrigerator, cooktop, oven, dishwasher, built-in microwave oven, and washer/dryer

Standard 203(k)

The Standard 203(k) can be used for larger remodeling and repairs, compared to the Limited 203(k).

There is a minimum repair cost — $5,000 — and the use of a 203(k) Consultant is required. As is the case with any 203(k) loan, the maximum amount is $35,000.

Eligible improvements include:

- Converting a one-family structure to a two-, three- or four-family structure

- Making changes for aesthetic appeal

- Creating accessibility for persons with disabilities

- Landscaping

Fannie Mae HomeStyle Renovation Loan

Another rehab loan option, the Fannie Mae HomeStyle loan is a conventional renovation loan that allows home buyers to finance the cost of purchasing and remodeling a home in the same loan.

Though it does have similarities to the FHA 203(k), there are many notable differences, the biggest of which is that while FHA 203(k) loans can only be used on primary residences, HomeStyle loans can be used on secondary homes or investment properties.

Because of this, and it’s stricter requirements, the Homestyle loan is regarded as a step up from the FHA 203(k) loan, but it is still available for first time home buyers who qualify.

Pros

- You can use the HomeStyle loan on any type of property, including vacation homes and investment properties. Unlike the 203(k) loan, there are no restrictions on property occupancy status.

- You can use the proceeds for any type of renovation, such as for luxury items like a pool.

- If you put down a 20% downpayment, you can avoid private mortgage insurance.

Cons

- Qualifying is more strict than an FHA 203(k): you’ll need at least a 620 credit score for a Fannie Mae HomeStyle loan.

- The renovations must be completed within 12 months of the closing date.

- Lenders must approve the contractors you hire.

- Since you have to hire a qualified contractor to perform most of the work, the amount you can do yourself is limited.

- Because Fannie Mae does not let just any lender sell the HomeStyle product, it can be difficult in some markets to find a lender who meets the specific requirements to offer the loan.

Alternative Options to Rehab Loans

Are there other options besides the FHA 203(k) and the Fannie Mae HomeStyle Loan?

There are, and next, we’ll look at alternative options to rehab loans.

As you explore each option, it’s important to think long term and how much each loan option will cost over the entirety of your loan — not just the initial cost.

While many of these alternative options can wind up being far more expensive than the rehab loans mentioned above, it’s important to see the full gamut of what is available for you.

Credit Card

Some homeowners may consider paying home renovations on a credit card. After all, it can be the easiest way — simply swipe and go.

If you have a credit card with a 0% APR for an introductory period and you are charging an amount small enough that you can pay off within a single billing cycle, then this is an option.

But creating a large balance on a credit card with a high-interest rate is a recipe for financial disaster.

According to recent Federal Reserve data, the average APR across all credit card accounts is over 15 percent — the highest rate recorded in the last 15 years.

If you put renovations on a credit card, you’ll be in danger of piling up high-interest debt that grows every month the balance isn’t paid.

Over time, you can end up paying tens of thousands more than you would have by utilizing a rehab loan.

Just to reiterate: unless it’s a small amount that you can pay off within a single pay period, and you have a long introductory 0% APR, we do not recommend using a credit card for a renovation.

Cash-out Refinance

Known as a mortgage refinancing option, a cash-out refinance is when a mortgage is refinanced for more than what is owed and the borrower takes out the difference in cash to then be used for renovations.

Here’s how it works: let’s say that you bought a home for $150,000 and you’ve paid off $50,000. You owe $100,000 on your home.

You want to make $25,000 worth of renovations.

Using a cash-out refinance, you would take an amount of your equity and then add what you’ve taken out onto your new mortgage principle.

This means your new mortgage would be worth $175,000 (the original $150,000 owed on the home plus the additional $25,000 you need for renovations), and your lender gives you the $25,000 in cash for renovations.

Home Equity Loan or Home Equity Line of Credit (HELOC)

A home equity loan or HELOC gives you the ability to withdraw a portion of your home’s equity in cash utilizing a second mortgage.

Keep in mind there are differences between the two.

A home equity loan is a lump-sum loan with a fixed rate. On the other hand, a line of credit acts similarly to a credit card and has a variable rate.

Personal Loan

Another option to pay for home renovations is personal loans. Personal loans typically have lower interest rates than credit cards, but often higher interest rates than rehab loans, costing you more in interest in the long run.

Rehab Loans: What’s Best For You?

While renovating a home can be difficult, choosing how to pay for it doesn't have to be.

Choosing from one of the rehab loan options comes down to what’s best for your financial needs.

Here are a few examples.

- If you’re wanting to buy and renovate an investment property, the HomeStyle loan is the obvious choice since the FHA 203(k) won’t pay for a property that isn’t your primary residence.

- If you have a low credit score, the FHA 203(k) loan may be your best (and only) option.

- If you’re only doing minor repairs, a Limited FHA 203(k) is a wiser move rather than utilizing a Standard FHA 203(k).

- If you don’t have reserve funds to pay for a large down payment, then an FHA 203(k) loan may be your best. On the other hand, if you can afford a large down payment and you have good credit (which can lower your interest rate), a HomeStyle loan is likely your better option.

- If you want to add luxury features to the house, such as a pool, you won’t be eligible for an FHA 203(k) loan, but you may be able to qualify for the HomeStyle.

Whether you choose the FHA 203(k) or FannieMae HomeStyle, ensure that you examine the total cost of the loan.

Most of all, stay away from accruing high-interest debt for home renovations — and for other personal finance needs.

Continued Learning: Rehab Loans

Now that you know more about what rehab loans are, as well as the types of rehab loans to choose from, don’t stop your home buying education there. Here are additional (and free!) WealthFit approved home buying resources:

- Use this strategy to buy a house with little to no money down

- Here are the pros and cons of buying a home without a realtor

- Learn how you can negotiate your mortgage rates

- Here is a guide to understanding HOA fees

- Use this home inspection checklist so that you don’t miss a thing

- How much money do you need to invest in real estate? Find out here