Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

- What Is Private Mortgage Insurance?

- Advantages and Disadvantages Of A Zero Down Mortgage

- 5 Ways To Buy A House With Little-To-No Money Down

- Tips for Buying a House With No Money Down

- Reasons To Do A Downpayment

- How To Buy A House With No Money Down: What’s Best For You?

- Continued Learning: Home Buying and Real Estate Investing

Let’s be honest: buying a home can be complex. There is often a lot of lengthy paperwork, required signatures, and unfamiliar terms.

One of the questions that many people have during the home buying process centers around what’s called the down payment, or the initial upfront payment. These questions include:

- How much should you put down?

- Should you put any money down?

- Do you have to put down 20%?

- Can you buy a house with no money down?

In this article, we’re going to discuss how to buy a house with no money down — or very close to it, along with:

- What private mortgage insurance is — and why it’s important

- Advantages and disadvantages associated with buying a house with no money down

- Specific programs that allow you to buy a home with no money down, along with programs that allow you to put down as little as 3%

- A look at the other side of the coin: the advantages of providing a large down payment

- Other home buying and real estate investing resources

Let’s get started!

What Is Private Mortgage Insurance?

You may be aware that most people recommend a 20 percent down payment. But did you know that’s not actually a requirement? It’s true.

Let’s explore the myth that a 20 percent down payment is required.

Where did it come from?

It stems from something called Private Mortgage Insurance (PMI). Private mortgage insurance is a requirement for those who borrow conventional loans with a down payment of less than 20 percent.

This insurance exists because it protects the lender in the event that a borrower defaults on the loan.

Mortgage insurance costs are included as part of the monthly loan payment, and it typically costs from 0.5%-1% of the entire annual mortgage.

Thus, if you take out a conventional loan and put down less than 20%, you are required to have PMI — which is where the 20% rule comes from.

Now that you know that the 20 percent recommendation isn’t a requirement, let’s look at the advantages and disadvantages of buying a house with a zero down mortgage.

Advantages and Disadvantages Of A Zero Down Mortgage

Before we explain how to buy a house with little to no money down, let’s first explore the advantages and disadvantages associated with it.

Advantages

Save Money Initially

The advantages are simple: you save money by putting less money down. WIth that money, you can:

- use it for expenses associated with the house

- pay off debt

Buy A Home Sooner

Along with that, because less money is needed to buy a home when you’re doing little to no money down, you can purchase a home sooner than you otherwise would be able to.

Programs To Take Advantage Of

There are several enticing no money down programs that you can take advantage of if you qualify, such as a 0% down VA loan if you are in the military.

Disadvantages

The disadvantages associated with buying a house with no money down include:

Higher Monthly Payments

Because you’re putting down less money upfront and borrowing more money, you will be paying more per month.

Paying PMI

In many cases, because you won’t be putting money down, you’ll be required to pay private mortgage insurance.

Little Equity

While many homeowners use home equity loans to help pay for items such as home repairs, you may not have enough equity to borrow, resulting in having to find other and more expensive high interest loans.

Danger in the Event of A Economic Downturn

In the event of an economic downturn, you could find yourself owing more money than your home is worth, or “being upside down”.

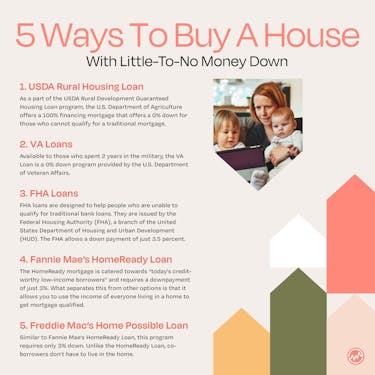

5 Ways To Buy A House With Little-To-No Money Down

Is buying a house with no money down right for you? Here are 5 ways to do just that.

USDA Rural Housing Loan

As a part of the USDA Rural Development Guaranteed Housing Loan program, the U.S. Department of Agriculture offers a 100% financing mortgage that offers a 0% down for those who cannot qualify for a traditional mortgage.

It’s not just for those living in rural areas; it’s available to buyers in suburban neighborhoods as well.

In 2017, as a part of its Rural Development program, the USDA helped some 127,000 families buy and upgrade their homes.

There are 3 types of programs offered from the USDA home loan:

Loan Guarantees

The USDA guarantees a mortgage issued by a participating local lender allowing you to get low mortgage interest rates, even without a down payment.

Direct Loans

Issued by the USDA, these direct loan mortgages are for low-income applicants.

Home Improvement Loans And Grants

These loans give homeowners the opportunity to repair or upgrade their homes. Packages can also combine a loan and a grant, providing up to $27,500 in assistance.

Eligibility

In order to be eligible for many USDA loans:

- household income must meet certain guidelines

- the home to be purchased must be located in an eligible rural area as defined by USDA

You can find out if you’re eligible here.

VA Loans

Available to those who spent 2 years in the military, the VA Loan is a 0% down program provided by the U.S. Department of Veteran Affairs.

Some key benefits of the VA loan are :

- You may use intermittent occupancy

- Bankruptcy and other derogatory credit do not immediately disqualify you

- No mortgage insurance is required

Find out if you qualify right here.

FHA Loans

FHA loans are designed to help people who are unable to qualify for traditional bank loans. They are issued by the Federal Housing Authority (FHA), a branch of the United States Department of Housing and Urban Development (HUD).

The FHA allows a down payment of just 3.5 percent.

Requirements include:

- Proof of reliable income

- your credit score requirement is only 500

- No bankruptcies within two years of your loan application

- A commitment of one year

To learn more about the FHA Loan Process, right here.

Fannie Mae’s HomeReady Loan

The HomeReady mortgage is catered towards “today’s credit-worthy low-income borrowers” and requires a downpayment of just 3%.

What separates this from other options is that it allows you to use the income of everyone living in a home to get mortgage qualified.

Requirements include:

- Low income. Your income must be at or below 80% of the area median income

- First-time or repeat homebuyers

- Limited cash for a down payment

- Credit score 620 or greater

- Supplemental boarder or rental income

- Looking to purchase or refinance

It also stipulates that if a borrower is a first-time homebuyer, homeownership education is required.

Learn more about the HomeReady mortgage here.

Freddie Mac’s Home Possible Loan

Similar to Fannie Mae’s HomeReady Loan, Freddie Mac’s Home Possible Loan program requires only 3% down.

Unlike the HomeReady Loan, co-borrowers don’t have to live in the home.

Requirements include:

- a minimum credit score of 660 for a fixed-rate mortgage and 680 for an adjustable-rate mortgage

- Low income. Your income must be at or below 80% of your area median income

To see if you qualify, learn more about Freddie Mac’s Home Possible Loan here.

Now that you know the programs available that will help you buy a house with little to no money down, let’s look at tips for buying a house with no money down.

Tips for Buying a House With No Money Down

There are ways to improve your chances of buying a house with no money down. Here are 3 of those tips.

Boost Your Credit

Your credit score isn’t just a random number; it is an indication of your willingness to pay back money that is borrowed or owed. Plus, having a good credit score increases your chances of buying a house with no money down.

For example, in order to qualify for the HomeReady loan, you must have a 620.

So how can you boost your credit score? Here are a few free resources:

- Use this strategy to improve your credit score in 30 days

- Here’s how to use a goodwill letter to boost your score

- Learn how to cancel a credit card without hurting your credit score

- You can improve your credit score by removing derogatory marks. Here’s how to get them permanently removed

- Become an authorized user to enhance your score

Know What You Can Qualify For

There are options when buying a house with no money down — maybe more options than you had anticipated.

That’s why it’s critical to know every option, and know exactly what you qualify for so that you can get the best deal.

Think Long Term

The key to buying a house with no money down — as well as mastering your personal finances and investing — is assessing your finances and thinking long term.

Buying a house with no money down to save money and expecting an increase in cash flow in the future can set you and your family up for financial stress.

Choose a mortgage that you can afford today — and in the future.

Reasons To Do A Downpayment

In order to decide whether or not buying a house with no money down is or isn’t right for you, let’s look at the advantages of a down payment.

Advantages Of A Down Payment

Lower Monthly Mortgage Payment

You can lower your mortgage payment with a downpayment.

Less To No Private Mortgage Insurance

This can keep you from paying private mortgage insurance, or paying less. Conventional mortgages only require PMI until the loan-to-value ratio has reached 80%.

Less Interest

By paying a downpayment, you will owe less of a balance, which is subject to interest. Because of this, you will pay less interest overall.

More Equity In Your Home Sooner

With a large down payment, you can pay off a chunk of your home — and build equity in it faster than if you didn’t buy a house with money down.

Increased Odds Of Getting A House In Multiple Offer Situation

If there are multiple offers on the same property, the person who’s offer is accepted may be the best offer — and one that includes a downpayment.

Because of this, you can increase the odds of getting a coveted house.

How To Buy A House With No Money Down: What’s Best For You?

Now that you know the intricacies of how to buy a house with no money down, should you? What’s best for you?

It depends upon your financial situation, as well as your financial goals.

If you’re looking to buy a home and pay the least amount possible, whether out of a low cash flow or desire, buying a house with no money down is a possibility.

But if you’re looking to buy a home and pay it off as soon as possible, it makes more sense to utilize a down payment.

Continued Learning: Home Buying and Real Estate Investing

Now that you know how to buy a house with no money down, continue your financial education with these free home buying and real estate investing resources:

- Find out how to buy a house without a realtor

- Use this article to decide if you should buy a property with HOA fees

- Did you know that you can negotiate your mortgage rate? Here’s how

- Use this home inspection checklist before you buy a house

- Interest in investing in real estate? Here’s a Beginner's Guide