A steady paycheck makes it easier to follow a budget and meet your financial goals throughout your career—but when you retire, pulling money from your savings or other investments as you need it can be stressful and a chore. What if you could create your own “retirement paycheck”? You can!

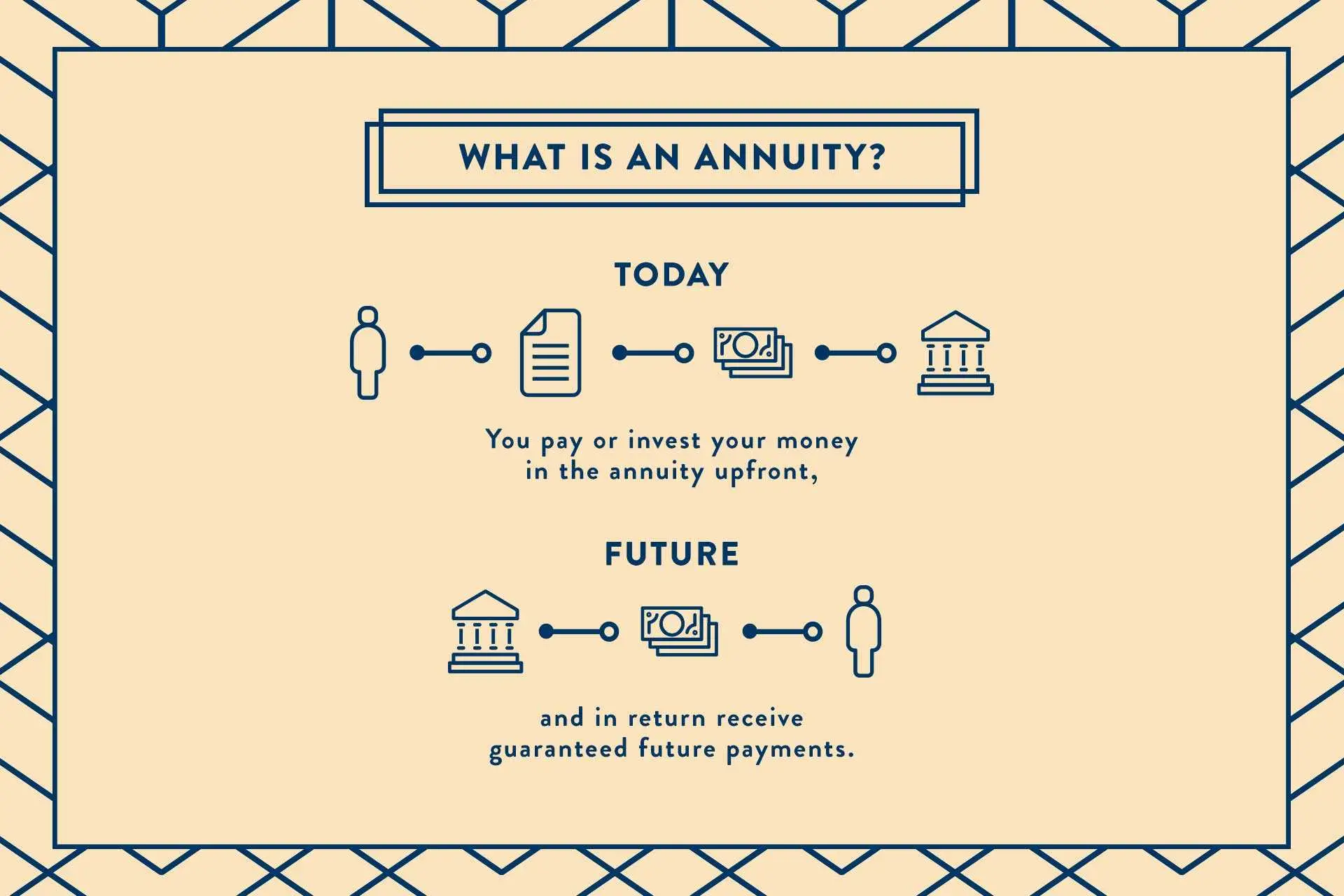

An annuity is a financial product that creates an insurance contract between you and an issuing party. You pay or invest your money in the annuity upfront, and in return receive guaranteed future payments.

Because life insurance companies offer annuities, they can supply levels of protection and guarantees you can’t always get from other financial products.

Of course, the quality and financial strength of the insurance company should be assessed to determine how much their guarantees are worth. This will be discussed more in depth later on.

How an annuity works is that it can be a supplemental stream of income—a “retirement paycheck”—to help diversify how you fund your retirement. But annuities aren’t right for everyone.

Read on to learn how an annuity works, their pros and cons, the different types of annuities available, how they are taxed, and how annuities compare to other investment vehicles to help you determine if buying an annuity is a smart decision for your finances.

How an Annuity Works

Purchasing an annuity involves entering into a contract with a financial institution, usually an insurance company, to provide you with a source of income during retirement.

Here’s how an annuity works: you make a lump sum payment or pay over time for the annuity, and the insurance company invests your money. The insurance company then makes regular payments to you in retirement, depending on the type of annuity you select and the terms of the product.

People choose annuities to help transfer the risk of living a long time—and needing money for decades after they retire—to the insurance company supplying the annuity.

With increasing life spans, fewer pensions, an uncertain future for Social Security, and people struggling to save for retirement, annuities can reduce the risk of making critical mistakes with your investments, such as emotions taking over in a volatile market.

But as you may have guessed, transferring risk also comes with a price tag.

If you have any concerns about a gap in funding your retirement and supporting your standard of living, keep reading to help determine if an annuity is a product right for you.

Pros And Cons Of An Annuity

Let’s look at the various advantages and disadvantages of how an annuity works as a tool to manage money in retirement.

Advantages of Annuities

Reliable Income In Retirement

Annuities are long-term financial products designed to protect you from the risk of outliving your money. Most people buy annuities to get regular payments for their lifetime.

Annuities can “bridge” the gap with other streams of income to meet your expenses each month in retirement. While distinct types of annuities exist, they all offer the buyer peace of mind when it comes to supplementing their income as they age.

Increase Tax-Deferred Retirement Savings

If you’ve contributed the maximum to your 401(k) or IRA, putting money into an annuity can increase your tax-deferred retirement savings. Annuities do not have annual contribution limits, and you won’t owe taxes on the growth in your account until you start collecting payments.

Guaranteed Interest, Death Benefits, And Inflation Protection

The various products or options you choose for an annuity will determine how an annuity works and which benefits are provided.

Fixed annuities guarantee the funds you deposit will be “safe” and that you’ll earn a specific amount of interest. Variable annuities don’t guarantee a rate of return but can offer more upside—with more risk.

If you want to insulate against rising prices in retirement, an inflation-protected annuity might interest you. More choices can better meet your individual needs, but they come with more cost.

Drawbacks of Annuities

Fees And Expenses

The notoriously high costs associated with how an annuity works may deter people from creating an annuity. Annual investment management fees, administrative fees, and mortality and expense fees are a few of the charges involved with specific annuity products. These fees can cost you 2-3% or more of your investment.

Purchasing extra guarantees (also known as riders) also come with steep costs. If you buy through a broker, you’ll also pay a hefty commission—often 10% or more.

Loss Of Liquidity And More Fees

Because of how an annuity works, when you buy one, you’re limiting access to your money. If you decide to withdraw money or transfer it to a different company during the surrender period (the early years of your contract), you’ll pay high surrender fees.

Once you start taking payments, your annuity may be irrevocable—meaning you may not be able to get your money back. It may be possible to move your funds into a different annuity. Just know you may face added expenses for doing so.

Annuity Products Are Often Misunderstood

Most people understand the basics of how an annuity works and that it can be part of the foundation of a secure retirement plan. But many annuities are complex and have many options and fees involved affecting their rate of return. This can cloud a consumer’s assessment of the product.

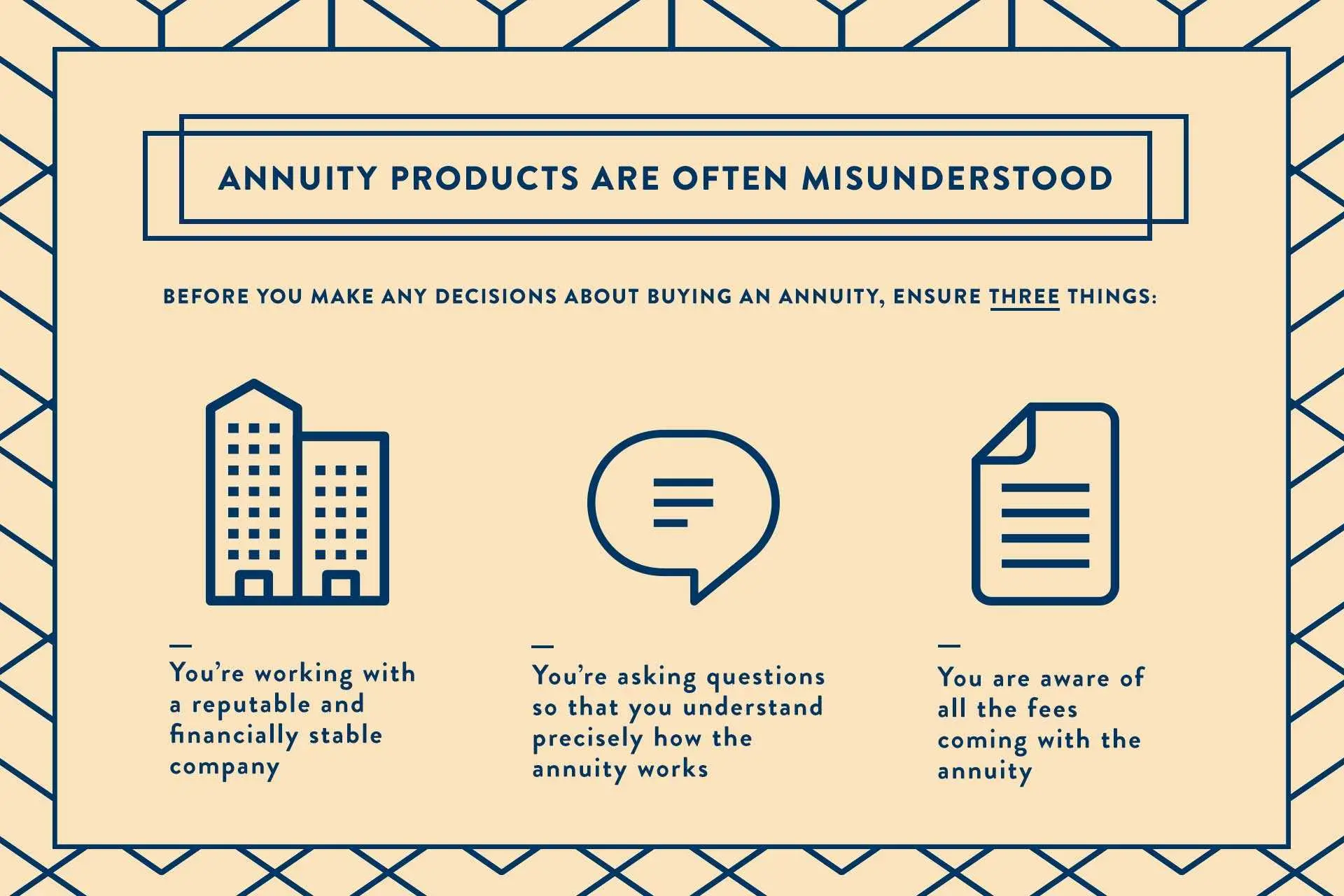

Before you make any decisions about buying an annuity, ensure three things:

- you’re working with a reputable and financially stable company

- you’re asking questions so that you understand precisely how the annuity works

- you are aware of all the fees coming with the annuity

Finally, consider buying direct-sold annuities from investment companies to avoid excessive fees. You’ll save on surrender charges and sales commissions when you buy a low-cost annuity from companies including Vanguard, Fidelity, Schwab, T. Rowe Price, and TIAA-CREF.

When Investing In An Annuity Makes Sense

Even with a better understanding of how an annuity works, you still might wonder when it makes sense to buy one. Going back to the idea of creating a “retirement paycheck” can help clarify when making an annuity purchase is the right decision.

When you’ve collected a paycheck for decades, giving up that stable income source in retirement can create anxiety and stress during a time in your life when you’ll already be adjusting to many changes.

Before you retire, you need to have a clear plan of your income sources during your retirement years.

You also need to know how you’ll fund your retirement lifestyle. Sources can include:

- savings and investment accounts

- pensions

- rental property income

- social security

If you have enough stable income sources to cover your monthly expenses comfortably, you probably don’t need to invest in an annuity—though it’s important to know how an annuity works in case you later decide to change strategies.

If one of the following conditions describe you though, an annuity can make sense:

Lack of Savings

If you’re concerned about how you’ll pay for retirement, or you realize there’s a gap to fill in creating your “retirement paycheck”, guaranteeing you an income for the rest of your life—which is how an annuity works—might be a good idea.

Uncertainty Over Expenses and the Market

If you plan to use your investment portfolio to fund your retirement, keep in mind some people access their money more often than they originally planned on. Plus, the market can be volatile, creating downturns in the market.

If you don’t track your expenses or use a budget, you might be surprised at how fast your financial account balances go down. You don’t want to outlive your money!

Inflating Lifestyle

Significant, unplanned spending early in retirement can cause severe financial stress years down the road.

With the average life expectancy increasing, annuities can help those who might inflate their lifestyle in retirement by helping them budget their money early on.

Types of Annuities

Annuities can come with fixed or variable interest rates, creating guaranteed fixed or variable payouts. They can also begin paying out immediate income or be deferred annuities.

Understanding these differences and how an annuity works combined with your income goals, risk tolerance, and the timeline for collecting payments will help you determine which annuity is best for you.

How Does An Immediate Annuity Work?

An immediate annuity, otherwise known as an income annuity, is usually bought by someone already in retirement or nearing retirement.

With just one lump-sum payment, an immediate annuity starts paying out a guaranteed income right away, or within one year of purchase. Payments continue for a set period, often until death.

Some of the drawbacks to an immediate annuity include:

- Benefits expire when you die unless you buy a rider to provide for beneficiaries

- Loss of access to the lump sum of money you paid to buy the annuity

- Monthly payments won’t increase to cover rising expenses unless you buy an inflation-protected annuity

How Does A Deferred Annuity Work?

A deferred annuity is a long-term retirement planning tool for those who don’t need money right away in retirement or those who are still working, but want another source of income in retirement.

This type of annuity has higher guaranteed monthly payments because payments are delayed by several years. You have the choice to pay a lump sum or a series of payments when buying a deferred annuity.

Additionally, deferred annuities can be converted to immediate income annuities when you’re ready to start collecting your “retirement paycheck”.

How Does A Fixed Annuity Work?

Fixed annuities are a popular choice because they guarantee your principal investment and a specific interest rate for a set number of years. While the interest you’ll earn is higher than most traditional savings vehicles, fixed annuities are considered conservative because they don’t offer growth opportunities.

For the most part, fixed annuities are simple and straightforward. Your earnings grow tax-deferred and many fixed annuities offer flexible rider options, including beneficiary protection.

You can convert your fixed annuity to an immediate annuity at any point to begin collecting a guaranteed income payout.

How Does a Variable Annuity Work?

Variable annuities give you more control over your investment dollars. They offer maximum stock market exposure through a range of investment options. These are popular options for people who are willing to embrace a higher level of risk in return for higher growth potential and potentially larger “retirement paychecks”.

Your account value varies based on the performance of the investment options you choose. While the investor’s principal is guaranteed, variable annuities also expose the owners to market risk, which means there’s no assurance of returns with this annuity type.

You can buy a variety of features with a variable annuity to customize the product to meet your needs. The riders—such as the one supplying a guaranteed lifetime income benefit—can provide some stability during market volatility. But they also come with higher fees.

Like fixed annuities, variable annuities also grow on a tax-deferred basis. Many also offer guarantees of at least your original contribution amount as a death benefit for beneficiaries should you die before starting income payments from your annuity.

How an Annuity Works with Income Taxes

Again, there is no tax benefit on the money you pay into an annuity. The interest you earn on your investment grows tax-deferred though—you won’t pay taxes on the growth until you start withdrawing those funds.

When annuity funds are distributed, you pay ordinary income tax on all gains. For many people, this tax rate is higher than the long-term capital gains rate they would have paid if they invested the money for more than a year in individual stocks or mutual funds.

If your employer offers the possibility of investing in an annuity through a traditional 401(k), your annuity payments are fully taxable as income.

Investing in an annuity through a 401(k) or a rollover to an annuity from a 401(k) or IRA account offers no added tax benefits because your original contributions and earnings are already tax-deferred.

Annuities Vs. Other Investment Vehicles

You know it’s important to diversify your investments in your retirement portfolio to help protect your finances. Now, after learning more about how an annuity works, you may question how they compare to other investment vehicles, such as mutual funds, bonds, and real estate investments.

Mutual Funds

Unlike mutual funds, annuities supply a guaranteed income. Some also guarantee a fixed level of growth—even in market downturns. But as stated before, these guarantees come with a cost.

The fees, commissions, and charges you pay for annuity products reduce the returns you’ll earn when compared with mutual funds. Mutual funds have the potential for higher returns but also carry more risk.

Bonds

Annuities and bonds both help minimize the risks involved with mutual fund investments. Because of how an annuity works—providing a regular payment guaranteed for life in exchange for the principal amount invested—payments often end when the annuitant dies.

Bonds generally pay higher yields and have lower fees and commissions. Buying bonds also gives you more flexibility because with bonds, you get your money back after receiving interest payments over a set period.

Real Estate Investing

The monthly income from real estate investments is similar to annuities because it can provide a diversified stream of income in retirement.

While there is risk involved in owning real estate, rental properties can also grow in value through appreciation. Variable annuities can also grow, while Fixed annuities cannot.

Something also to remember is that if you can find a trusted property manager, real estate investments can be mainly passive.

Final Thoughts How An Annuity Works

If you’re worried about running out of money in retirement or want to protect your retirement savings, it’s essential to consider every option available.

Creating your own “pension” with an annuity and getting guaranteed payments for life can fill the gap in covering your retirement expenses. This could solve your financial concerns, helping you sleep better at night.

Remember, annuities come with costs and are not right for everyone. If you choose to buy an annuity, it should be part of a carefully designed retirement plan.