Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

- What Is A Pay for Delete Letter?

- How Do Collections Affect Your Credit?

- How New Credit Scoring Models Minimize Collection Damage

- How To Create A Pay for Delete Letter: 4 Steps

- Pay For Delete Templates

- Pay For Delete: Frequently Asked Questions

- Alternative Ways To Have Collections Removed From Your Credit Report

- The Bottom Line: Pay For Delete

Do you have a collection account dragging down your credit score? You may think that paying it will remove it from your credit report. But paying off a collection account may not erase the damage. Depending on the type of collection account, it can stay on your credit report for 7 years.

That’s a long time, especially when you’re eyeing a car or mortgage loan.

That’s where what’s called a “pay for delete” comes in.

If you can get a collection agency to agree to delete the negative account from your credit report completely after you pay it (or a portion of it), your credit score could increase, allowing you to qualify for the loan you’ve been wanting.

Does a pay for delete letter really work?

More importantly, will a pay for delete letter help your current situation?

In this article, we’ll explain:

- What a pay for delete is — and how you can utilize it to fix your credit

- Free pay for delete letter templates that you can utilize

- Additional ways to improve your credit score instead of using a pay for delete letter

If you’re ready to improve your credit score, let’s get started!

What Is A Pay for Delete Letter?

A pay for delete letter consists of asking a creditor to remove a collection account or any other negative item from your credit report in exchange for paying a portion of the balance or in full.

It can be used when you owe a balance that cannot be disputed.

Keep in mind that if you’ve already paid the debt and you’d like the negative item removed, using a pay for delete letter won’t work. Instead, try a goodwill letter.

How Do Collections Affect Your Credit?

First, you must understand how creditors interpret collections — and how a pay for delete letter can then help. When you get sent to collections, creditors assume you will never pay the debt and this is reflected in lowering your credit score.

You should avoid these serious deductions by paying your debts on time.

There is also variability in how credit reports classify your missed payments. Usually, your debt is classified as late in the following parameters:

- 30 days

- 60 days

- 120+ days

The later a payment is, the worse it is for your credit. But if you already have a collections issue affecting your credit, the good news is that a pay for delete letter can help.

How New Credit Scoring Models Minimize Collection Damage

New credit scoring models are changing how they factor debt that goes to collections. Collection accounts influence your credit score less in 2022 because not everything on a credit report affects your credit score.

Here are a few examples of how new credit scoring models minimize collection damage:

- FICO 9 and VantageScore 4.0 do not grant the same significance for medical collections

- Medical collections are no longer the same as being considered reckless with money

- Credit reporting bureaus are not factoring small collections under $100 in the new credit scoring models

But, these new models are not widespread.

While we should see financial institutions and lenders convert to these more progressive models in the future, a pay for delete letter remains a good option for removing a collection account.

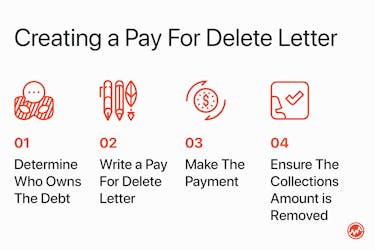

How To Create A Pay for Delete Letter: 4 Steps

If you owe a balance and you’re ready to try a pay for delete letter to fix your credit, here’s the 4 step process for doing so.

Step 1: Determine Who Owns The Debt

The first step is to find out who your letter is going to be mailed to. That’s why you need to find out who owns the debt: does the original creditor own it? Or a collections company?

Keep in mind that if a debt is delinquent, such as 60-90 days late or more, companies sometimes sell that debt to collections agency who then tries to obtain a portion of it.

Other times, the collections agency works as a middleman for the company and is paid a percentage when the debt is collected.

This is the case for any kind of debt, including:

You can find out which debt collector owns the debt by looking at your credit report — it will most likely be listed.

If that doesn't work, you can contact the company you originally used for services or a loan.

Step 2: Write A Pay For Delete Letter

The next step is to write a pay for delete letter. No, you don’t have to come up with it entirely on your own. There are free pay for delete templates below.

Keep in mind that it’s best to personalize the letter to your situation.

Step 3: Make the Payment

If the collection agency accepts your pay for delete offer, ensure that you have their response in writing, and send them a check by mail.

Step 4: Ensure The Collections Account Is Removed

Monitor your credit report to ensure that the negative item is removed.

If not, follow up with the company and remind them of their written agreement with you.

Pay For Delete Templates

If you want to write a pay for delete letter, here are a few templates that you can utilize.

In general, ensure that you include the following in the template:

- Your name

- Your address

- Collection agency's name

- Collection agency's address

- Account number

- Alleged amount owed

- Detailed description

Here's a pay for delete letter example.

(Account Number: XXXXXXXXXXX)

(Original Creditor: (creditor name))

(Amount as Listed on Credit Report: $XXXX.XX)

Dear [Creditor],

I am writing this letter to offer your credit department the one-time offer to settle the alleged amount owed. I do not acknowledge any liability for this debt in any form and I retain my right to request a full and complete debt validation from your company.

I am willing to pay $XXX.XX of this account if you agree to the following:

- Your company will delete all references to this account from my credit profile at the three credit reporting agencies.

- Your company will accept this payment to satisfy the debt in full.

- You will make no mention of this agreement to outside third parties.

If the above-mentioned items are met, I am willing to make payment on this debt.

I require your written agreement to these terms on company letterhead and signed by a representative who is authorized to enter into such agreements.

I look forward to your response.

You can contact me through any of the following methods.

(E-Mail Address)

(Phone Number)

Sincerely,

(Your Name)

If you’d like to see a few more templates, here are others you can utilize:

- Pay For Delete Template 1

- Pay For Delete Template 2

- Pay For Delete Template 3

- Pay for Delete Template 4

- Pay For Delete Template 5

It’s important to note the tone of a pay for delete letter versus other types of credit repair letters, such as a goodwill letter.

With a pay for delete letter, you are not kindly asking; instead, you are offering them the opportunity to earn money. It’s a mutual benefit.

Because of this, be bold and strict in your writing, especially when discussing the terms.

Excellent negotiation is the key to a pay for delete letter and can improve your chances of it being completed.

Pay For Delete: Frequently Asked Questions

Q. Is Pay For Delete Legal?

The short answer: Yes.

The long answer: While deleting a paid collection account is legal, keep in mind that collection agencies sign agreements with the credit bureaus saying they won’t delete negative accounts simply because they’re paid.

Because of this, if a collection agency accepts a pay for delete offer, they may be in violation of the service agreement with credit bureaus. Thus, the practice is deemed “shady”.

That being said, with a pay for delete letter, you’re giving a collection agency the financial incentive to look at your account, which might persuade them to bend the rules and take action.

Q. Does Pay For Delete Letters Really Work?

Because a pay for delete letter isn’t standard practice, collection agencies are under no obligation to grant your request.

But that doesn’t mean you can’t try. You will not be penalized in any way for sending a pay for delete letter.

Q. Does Pay For Delete Increase Your Credit Score?

Yes. By removing a negative mark from your credit report, your score can potentially increase the amount of points it originally decreased when the mark was placed on your credit report.

Q. How Much Should I Offer On A Pay For Delete?

While there is no set number, and it can vary on a case by case basis, Creditful.com recommends offering “40% to 50% of the debt for newer accounts, and 30% to 40% of the debt for older accounts.”

Q. Is Pay For Delete Outdated?

Newer credit scoring models — specifically VantageScore 4.0 and FICO 9 — actually do the pay for delete for you.

According to Creditcard.com, the new FICO 9 scoring model “doesn’t negatively rank paid collections of any type in your score and gives less weight to unpaid medical collections.”

While this is good news, the catch is that newer scoring models are not widely used — the common one is FICO 8 — and it will take time before this is fully implemented.

Thus, the pay for delete is not outdated in 2022 — and may be worth your time if you’re trying to help your credit score.

Q. What are debts that don’t require pay for delete to remove credit damage?

Some debts don’t require a pay to delete collections to remove credit damage. This includes:

- Defaulted student loans: by making nine payments in a row in ten months, you can get this off your credit report.

- Medical collections paid by insurance: Often, processing errors lead to medical bills going to collections. Once you have the situation straightened out with insurance, you can get these collections removed from your credit history. They do not require a pay for delete letter.

Q. What happens if a pay for delete letter is rejected?

There are instances when your pay to delete collections letter will be rejected — not all collection agencies will agree to your terms.

If they do accept your offer, make sure you communicate in writing. Verbal agreements are hard to prove if something falls through.

If an agency rejects your pay for delete letter, you still have options to delete the collections.

Alternative Ways To Have Collections Removed From Your Credit Report

There are other ways to have a negative item removed from your credit report.

Dispute the Account

According to the Federal Trade Commission, one in five people have an error on at least one of their credit reports. That 1 could be you.

Because of The Fair Credit Reporting Act (FCRA), you’re allowed to dispute items such as:

- Balances that seem incorrect

- Dates that seem incorrect

- Anything on your credit report that appears wrong or fraudulent

- Anything on your credit report you wish to have verified

If you find an error on your credit report, or simply want to dispute something that is unverified, you can use a 609 credit repair letter to do so.

Write a Goodwill Letter

A goodwill letter consists of you writing to your creditor and asking them to remove a negative mark on your credit report that you have already paid.

Although creditors don’t have to grant your request, writing the letter is simple and can’t hurt your credit.

Keep in mind, if there is an erroneous late payment on your credit report, you should dispute it, not write a goodwill letter.

Learn how to write a goodwill letter right here.

The Bottom Line: Pay For Delete

How do you remove paid collections from a credit report?

You have options.

The first step is to find the debt and write a pay to delete collections letter to get it off your record. This effort will pay off in the long run when you’re able to get approved for future loans, mortgages, and other major purchases.

Don’t let an old blemish on your credit report stop you from achieving your financial goals.

Pay to delete collections today.