Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

Anthony and Mark are both business owners in California. Though they live in different areas in the Golden State and have never met, they have striking similarities. Family men at heart, they both are business owners in the same industry, and both have a similar revenue each year. They have similar incomes and are in the same tax bracket. Each year, when they file their taxes, Anthony saves hundreds, sometimes thousands more than Mark. If they have so many similarities, what’s the difference? Anthony is following the “Pay Less Tax” blueprint and knows how to pay less taxes.

The truth is that you’re not a victim to the IRS; you can have a say in how much tax you pay. There are a number of lesser-known strategies that you can use to reduce the taxes that you owe each year.

Tom Wheelwright, Rich Dad Tax Advisor put together a blueprint on how to pay less taxes — legally. It’s called Pay Less Taxes: How To Legally Reduce Your Taxes By Up To 40%.

It includes two fundamental items:

- deploying lesser-known yet powerful tax reduction strategies

- a shift in mindset about how you view the IRS

We’ll dive deep into both fundamentals in this article.

But before we discuss how to pay less taxes, it’s important to understand that there’s only one way to so, and that’s to reduce your tax bill. If you refuse to file and pay your taxes, you can face serious legal consequences.

The Pillars of Tax Advantages

Before we wade into the Pay Less Taxes blueprint, it’s important to understand a few tax fundamentals.

Not only does your amount of income dictate how much taxes you pay; your source of income also impacts the amount of taxes that you pay.

Let’s examine the latter — how the source of your income — impacts your tax bill.

Self-employed

If you are self-employed, you pay both personal income taxes and business taxes, meaning they tend to pay more taxes than employees.

Employees

Employees pay income taxes on their wages.

Business Owners

Business owners typically pay fewer taxes than employees or self-employed.

Investors

Investors can significantly reduce their tax bill and pay the least amount of taxes.

The Tax Benefits of Becoming A Business Owner or Investor

Overall, the tax code primarily serves as a list of incentives. Certain deductions incentivize taxpayers to act or do business in certain ways.

Currently, the tax code offers more incentives for business owners and investors than employees or the self-employed, so it provides an incentive for people to act as business owners or investors.

Understanding these incentives that exist in the tax code and the tax advantages that are available will help you pay less taxes legally.

If you are able to shift from an employee to a business owner or investor, you’ll reap benefits every tax season.

Keep reading to find out how.

How To Pay Less Taxes

Strategy #1: Maximize Deductions for Business Owners

If you own a business or become a business owner, there are four keys to maximizing deductions so that your tax bill decreases.

You can deduct items that you purchase for your business, but they must meet the following requirements:

- business purpose

- typical or ordinary

- necessary

- documented

We’ll look at each one in-depth next.

Business Purpose

In order to deduct an item from your business income, it has to be purchased for a business purpose.

For example, you can’t buy a car for personal use and deduct it from your business taxes. However, if you buy a car for business use, it may be deductible. As long as your business has a reason to use the item that you purchased, it has a business purpose.

Typical or Ordinary

Purchases made for your business must be “typical or ordinary” in order to be deductible.

This means that both the product or service that you buy and the amount that you pay for it must be typical. For example, the expenses a salesman incurs who brings clients out to dinner and/or travels can be considered deductible.

Necessary

Necessary means that the purchase you made advances your business towards its goal of making money.

Returning to the example of going out for a meal: if you bring yourself or your family out to dinner, this is not necessary for advancing your business.

If you bring your business partner to dinner and discuss your business and ways to grow it, it can be argued that it was a necessary meeting that is deductible.

Documented

When you want to deduct something from your taxes, the most important thing is that you have documentation showing:

- what you purchased

- why you purchased it

- how much you paid

- why it is necessary

The easiest way to do this is to save receipts and write a short note on it about what you bought and why.

If you deduct a meal, write down what you talked about. If you buy a computer, note what the business purpose is. It may be hard to remember what each expense was for months later.

If you do have documentation, you can deduct the expenses because you have proof that it is a valid, deductible expense.

Strategy #2: Explore Underutilized Tax Brackets

Knowing how to use tax brackets is another key pillar for understanding how to pay less taxes.

In the US, there are seven tax brackets that range from 10% to 37%. The more you earn, the more taxes you pay. Everyone in the United States has these tax brackets, from billionaires like Warren Buffet all the way down to an infant child who can’t work.

Ensuring you keep most of your income in the lower tax brackets helps keep more money in your pocket.

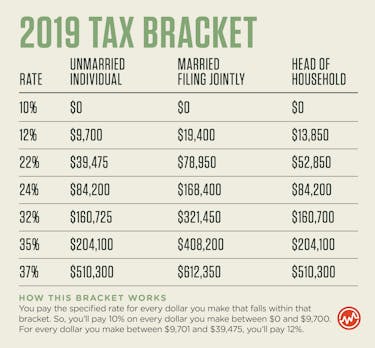

2019 Tax Bracket

Source: IRS

How The Tax Bracket Works

You pay the specified rate for every dollar you make that falls within that bracket. So, you’ll pay 10% on every dollar you make between $0 and $9,700. For every dollar you make between $9,701 and $39,475, you’ll pay 12%.

Just because you made $10,000 doesn’t mean you pay 12% on all $10,000. You only pay the higher rate on the amount you make in that bracket. You keep paying the 10% rate on all of your income between $0 and $9,700. Taxpayers can also take the standard deduction of $12,000. ($24,000 for married, filing jointly.)

This adds a 0% tax bracket on income between $0 and $12,000. That pushes the 10% bracket to $12,000 to $21,700, the 12% bracket to $21,701 to $51,475, and so on.

If you own a business, you’re well-positioned to utilize these tax brackets by minimizing the amount of income that falls into the higher tax brackets. Next, we’ll look at a specific example of how to do just that.

Saving $2,200 By Utilizing the Tax Brackets

Consider the following scenario. You earn $70,000 each year through your business. After subtracting out the $12,000 standard deduction, you earn $58,000 per year in taxable income. That puts $18,525 of your income in the 22% tax bracket.

You have a child who does not work. You can employ your child in your business doing anything from serving as a mascot to filing paperwork. You can pay your child for the service. If you pay them $10,000 over the course of the year, your income falls to $60,000 and theirs grows to $10,000. You only have $8,525 of income in the 22% tax bracket and they have $10,000 that all gets deducted through the standard deduction, meaning they owe no tax.

You can place the money you pay your child in a trust on their behalf, have them contribute it to an IRA, or otherwise have them save it for the future. Your child also gains valuable work experience.

By shifting your income in this way, you’re setting up your child for success in the future AND you save $2,200 in taxes. It’s a win-win.

Keep in mind, you cannot pay your child $1,000 per hour for menial office work. You have to pay a reasonable rate based on the market rates for the work that they do. Still, this can be an effective strategy for reducing your tax burden.

Strategy #3: Create A Team

Even though it may sound counterintuitive, creating and paying a team can actually help you save money.

You are the most important member of your team because you are the person responsible for making decisions regarding your money and who you add to your team.

While your team should be composed of people who can help you run your business and manage your money, you should be the one responsible for the final decisions.

Bookkeeper

The second most important person on your financial team is your bookkeeper. Your bookkeeper knows the numbers and keeps them accurate.

To pay less taxes, you must have accurate numbers for your income and your deductions. You also have to have documentation for everything. Your bookkeeper is responsible for keeping everything documented and accurate.

Tax Advisor

You also need a tax advisor. A good tax advisor knows the details of the tax code. They analyze your books and identify opportunities for you to reduce your tax burden by adjusting your expenses and deductions.

Your tax advisor should be in close contact with your attorney, who helps handle any legal issues your business may face.

Banker

Finally, you need a banker. Your banker should talk to your tax advisor and attorney, but not your bookkeeper. Your banker should be available to help you raise money for your business to fuel growth.

You need to pay your bookkeeper, tax advisor, and other members of your team, but if you choose the right team members, you should not see paying them as an expense. They should actually increase your income by reducing your tax liability.

Paying a tax advisor $1,000 a year to reduce your taxes by $1,500 doesn’t cost you anything — it makes you $500.

Strategy #4: Eliminate Fear and Take Appropriate Deductions

Many business owners hesitate to take certain deductions that they see as red flags for the IRS. The reality is that this fear can prevent you from paying less taxes.

According to Wheelright, one of the deductions most commonly seen as a red flag is the home office deduction. (In this case, ensure that the room is used ONLY used as a home office — and nothing else.)

Seeing something as a red flag for an audit means that you’re afraid of an audit. This is a reasonable fear, but the IRS shouldn’t be something to fear. The IRS should be your partner. If you’re audited, it’s a valuable opportunity to learn how your bookkeeper can better document your business or how your tax adviser can correctly identify tax-savings opportunities.

Even if you have to pay extra money to handle an audit, the savings from taking more “aggressive” flag-raising deductions will likely more than cover the cost.

Bonus Strategy: Advanced Deduction Strategies

Aside from these pillars, there are other advanced strategies that business owners can use to save even more money on their taxes.

One example is retirement contributions. Business owners can contribute to their own retirement accounts as both the business-owner an employee that is paid by the business. This turns the standard $19,000 401(k) contribution limit into a limit of $54,000 for business owners.

Business owners also have an advantage when it comes to deducting travel expenses. You cannot deduct commuting costs from your taxes, even if you’re traveling from your home to your first client meeting of the day. If you have a home office, your commute is the distance from your bedroom to your home office. You can then deduct your car ride to a client because you’ve already commuted.

The situations aren’t applicable to everyone, but your tax advisor can help you identify opportunities like this and document them properly to take advantage of the deduction.

How To Pay Less Taxes

If you shift your mindset, educate yourself, and embrace taxes . . . the benefits can be TREMENDOUS.

Watch Pay Less Taxes: How To Legally Reduce Your Taxes By Up To 40% for further explanations on the tax reduction strategies mentioned in this article and more.

The best part of this blueprint? There’s no sneaky stuff. It’s all legal.