Get Access to 250+ Online Classes

Learn directly from the world’s top investors & entrepreneurs.

Get Started NowIn This Article

Wondering how to get out of a car loan?

Buying a car doesn’t always work out the way you planned.

Many people have walked out of an auto dealership with more of an expensive vehicle than they intended to purchase...This may have even happened to you.

What can you do if you find yourself with a bad auto loan or a monthly payment you can’t afford?

Whether the new car smell is still fresh or even if you’ve been making loan payments for a few years, you might eventually find yourself wondering how to get out of a car loan.

You might even be underwater on the loan, meaning that our car is less than how much you owe.

Here’s the good news: you have options when trying to get out of a car loan

Here’s the bad news: getting out of a bad car loan might not be easy.

Read further to learn:

- how to get out of a car loan

- how credit affects the amount of interest you pay on a loan — and how to improve your credit

- how to avoid getting in a bad car loan in the future

5 Ways to Get Out of a Car Loan

Option 1: Refinance

The best option for getting out of a bad car loan might be to refinance the debt.

Once you make sure your current loan doesn’t charge a prepayment penalty (a fee that you will have to pay if you pay back your loan before it is due), you can start shopping around with new lenders for a better rate.

The better the condition of your credit reports and scores, the more money you may be able to save.

It’s also smart to restrict your rate shopping to a 45-day window so multiple hard credit inquiries will only count against your credit score once.

Option 2: Trade-In the Car

Unless your car loan is upside down (which means that you owe more than the vehicle is worth), you might consider trading your vehicle in for a different set of wheels.

If you can swap out your car for a lower-priced car and reduce your overall auto debt, that’s a bonus that could ramp up your potential savings.

Option 3: File Bankruptcy

Filing for bankruptcy is often considered a nuclear option when it comes to debt. A bankruptcy may protect you from your creditors (including your auto lender), but it can take a toll on your credit at the same time.

Bankruptcy may also make it difficult to borrow any money again in the future, at least at a decent interest rate.

Bankruptcy may not automatically get you out of your auto loan either unless you file a Chapter 7 and surrender the vehicle.

A bankruptcy attorney can discuss other options with you concerning your auto loan.

These might include making your regular payments (reaffirming the debt), getting a reduced payment, or paying the loan off in a lump sum.

Option 4: Surrender the Vehicle

If you’re considering surrendering your vehicle to the lender, read this first. Surrendering your vehicle is generally a bad idea for multiple reasons.

Giving back the vehicle doesn’t erase your debt and it doesn’t get you out of the promissory note you signed when you took out the loan.

Even if the lender sells the vehicle to someone else, you’ll still probably end up owing a balance — maybe a big one.

At that point, you might have to settle the debt or risk being sued by the lender.

Worst of all, surrendering a vehicle could be horrible for your credit score.

A repossession (voluntary or involuntary) may damage your credit scores. Having a repossession noted on your credit reports may also make it hard to borrow money again down the road.

Option 5: Swap Your Lease

Another way to get out of a car loan: It might be possible to swap your car lease.

Some auto leases allow for a third-party transfer, but not all.

If your lease allows you swap it out, you have a couple of options.

You can swap the lease with a friend or family member.

You can also create an account on a lease swapping website.

If you choose to swap your auto lease online, you will need to provide specific information about the vehicle. You also need to let the potential buyer know details about the lease, including monthly payment amounts.

After the potential buyer is approved by your leasing company, you complete the paperwork and turn over the vehicle’s keys.

The leasing agent arranges the swap, and you no longer need to worry about making the monthly payments.

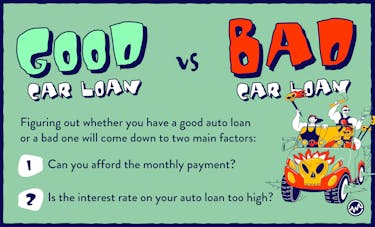

Do You Have a Good Or Bad Car Loan?

How can you know if your loan is truly a bad one? How can you decide between a good or bad loan?

Figuring out whether you have a good auto loan or a bad one will come down to two main factors:

- Can you afford the monthly payment?

- Is the interest rate on your auto loan too high?

Evaluating whether you can afford your monthly car payment requires some digging and an honest look at your monthly budget.

While knowing if you can afford the monthly payment is pretty straight forward, knowing if your interest rate is too high isn’t.

So how can you tell?

Good and Bad Interest Rates

According to Experian, below are the average interest rates you might expect to pay for an auto loan, based on your credit score range.

Sometimes people get into bad car loans without understanding the impact a high APR can have on their finances.

Your APR and the length of your loan ultimately decide the size of your monthly payment — however high or low that may be.

Not only that, but a high APR could cost you thousands of extra dollars for the same vehicle.

Here’s a quick illustration that shows how APR can affect the cost of your loan.

For example, with a 20.99% APR (versus 4.77%), you’d pay:

- $195 more per month

- $11,667 in extra interest over the loan

How Your Interest Rate Is Decided

As you can see, your credit score is a huge factor in the price you pay for an auto loan.

Are you likely to pay on time? Or are you likely to pay late, or worse, default?

Lenders answer these questions by checking your credit score.

Look at it this way. Let’s say you have a friend who asks to borrow $500. Your friend is responsible, trustworthy, and has a job. You believe he’ll pay you back as promised. So, you loan him the money.

Lenders can’t make decisions this way. They don’t know you personally, so they can’t use gut instinct to decide whether to loan you money.

Instead, they rely on your credit to help fill in the blanks.

How Credit Scores Predict Risk

Credit scores are created for the following purpose: they analyze your credit report and predict the likelihood that you’ll pay any bill 90 days (or more) late within the next 24 months.

If your credit score is low, it tells the lender that doing business with you is a greater risk.

When a lender checks your credit and thinks loaning money to you could be risky, they will charge you a higher interest rate to help make up for the risk it’s taking.

If your credit is too damaged, your application for a loan will likely be denied.

How to Know If You Have a Bad Car Loan

Take a moment to put yourself in a lender’s shoes. It’s understandable that lenders may need to deny applications or charge more money if they’re less likely to get repaid as promised.

If they didn’t, everyone would pay higher rates.

You might not be willing to loan personal money to someone you aren’t sure would pay you back either.

But sometimes, lines are crossed. Certain lenders might charge you more than is fair for your credit score. Auto dealers themselves might also mark up your interest rate, even if you qualify for a lower one, to try to make more money.

Here are two signs that you may be stuck in a bad auto loan.

- Your interest rate is higher than the average interest rate for your credit score range.

- Your credit has improved since you took out the loan.

Technically — in example #2 above — you might not be in a bad loan.

Your lender may have offered you a fair rate when you applied for financing.

But if your credit has improved since then, it may be a sign that you’ve outgrown the loan.

How to Avoid A Bad Car Loan In The Future: 6 Ways

Before you finance your next vehicle, here are tips that will help you avoid wondering how to get out of a car loan in the future.

#1: Improve Your Credit

Lenders base interest rates primarily on your credit report and score. If you want to secure a good auto loan, your best bet is to work hard to improve your credit before you apply for financing.

Here are a few free resources to improve your credit score:

- Learn how to improve your credit in 30 days using this strategy

- Try this free and easy credit repair tactic

- Here are goodwill letter templates you can use to boost your credit score

- Should you buy tradelines to improve your credit score? Here’s what you need to know

#2: Shop For The Best Rate

Don’t be impulsive! Jumping into a vehicle purchase and financing head-first can be a recipe for disaster.

Instead, take the time to compare offers (and vehicles) from several different lenders before you commit to a loan.

#3: Pay In Cash

Most people don’t purchase vehicles in cash, but it’s possible. You could start a dedicated savings account now and funnel money to it every month.

When the time comes to buy a new vehicle, you might be able to find a good deal on a used vehicle and pay in cash so that you don’t need a loan at all.

#4: Estimate The Cost Over Time

Keep in mind that you’ll pay more than the sticker price for a car over time. Other fees come with a car — such as:

Ensure that you can still afford the vehicle along with these additional costs.

#5: Understand the Length Of Your Auto Loan

Payment plans from banks and credit unions often range from 24 to 72 months. According to a recent survey, the typical term length for auto loans is 63 months, with “loans of 72 and 84 months becoming increasingly common.”

While a longer auto loan can equate to a cheaper monthly payment, it extends the amount of time you’re paying interest. Plus, if you expect to put high mileage on the vehicle, you may need a new car before the car is paid off in 5.25 years.

#6: The Dangers of No Downpayment

Some car dealerships tout a “no money down” deal. While this may seem good at the outset, it can lead to problems down the road in the form of high monthly payments with interest.

A good rule of thumb is to make a down payment of at least 20% (if you can’t pay full in cash) so that you can reduce the cost.

How To Get Out of a Car Loan: Frequently Asked Questions

Next, we’ll look at some of the most commonly asked questions associated with how to get out of a car loan.

Q. Does giving a car back hurt your credit?

You can expect your credit score to drop several points after you surrender a leased vehicle.

The amount your score drops can range between 50 to 150 points.

It can be a big hit, especially if your credit rating is already low.

The reason for the ding to your credit rating is due to the failure to honor the terms of the lease.

Before you decide to return the vehicle to the leasing agent, it’s always a good idea to see if you can work out an arrangement.

It may extend the lease, but you don’t have to worry about a negative impact on your credit score.

Q. How can you get out of a car loan without penalty?

You have a few options when you need to get out of a car loan without incurring any financial penalties.

Paying off the loan is the best solution, but not everyone has the extra cash necessary to settle the lease.

Another option is to inquire about refinancing the loan.

Most lenders prefer refinancing to taking possession of the vehicle.

You can also sell the car and use the proceeds to settle the loan.

Voluntary repossession is another way you can get out of a loan, but it may come with penalties that can affect your credit score.

Q. Can you back out of a car loan?

The short answer is no, you cannot back out of a car loan.

The lease is a legally binding agreement between you and the financier.

Most states have laws in place that protect both the buyer and seller that includes the lease agreement.

The only time you can back out of a signed car loan is if the vehicle falls under your state’s lemon laws.

The Bottom Line: How To Get Out Of A Car Loan

Remember, it’s easier to avoid a bad car loan in the first place than it is to try to get out of one after you’ve signed on the dotted line.

Avoid one at all costs. And, if a friend or family member starts to wonder how to get out of a car loan, be sure to share these tips with them so that they can avoid the process.

Now that you know how to get out of a car loan, continue your debt strategy education with these free resources:

- Learn how to get help with medical bills

- Utilize this strategy to consolidate credit card debt

- Discover the difference between good debt and bad debt

- Follow these 11 rules if you’re marrying someone with student debt